Corporate tax rules are shifting faster than many finance teams can update policies. The most “future-proof” businesses in 2026 aren’t trying to predict every new rule—they’re building a repeatable tax governance system: scenario planning, strong documentation, controllable data, and a structure that can flex as rules change. This is where Xerosoft Global can be positioned as a strategic partner—helping companies modernize tax planning, reporting readiness, and audit resilience.

Key Benefits

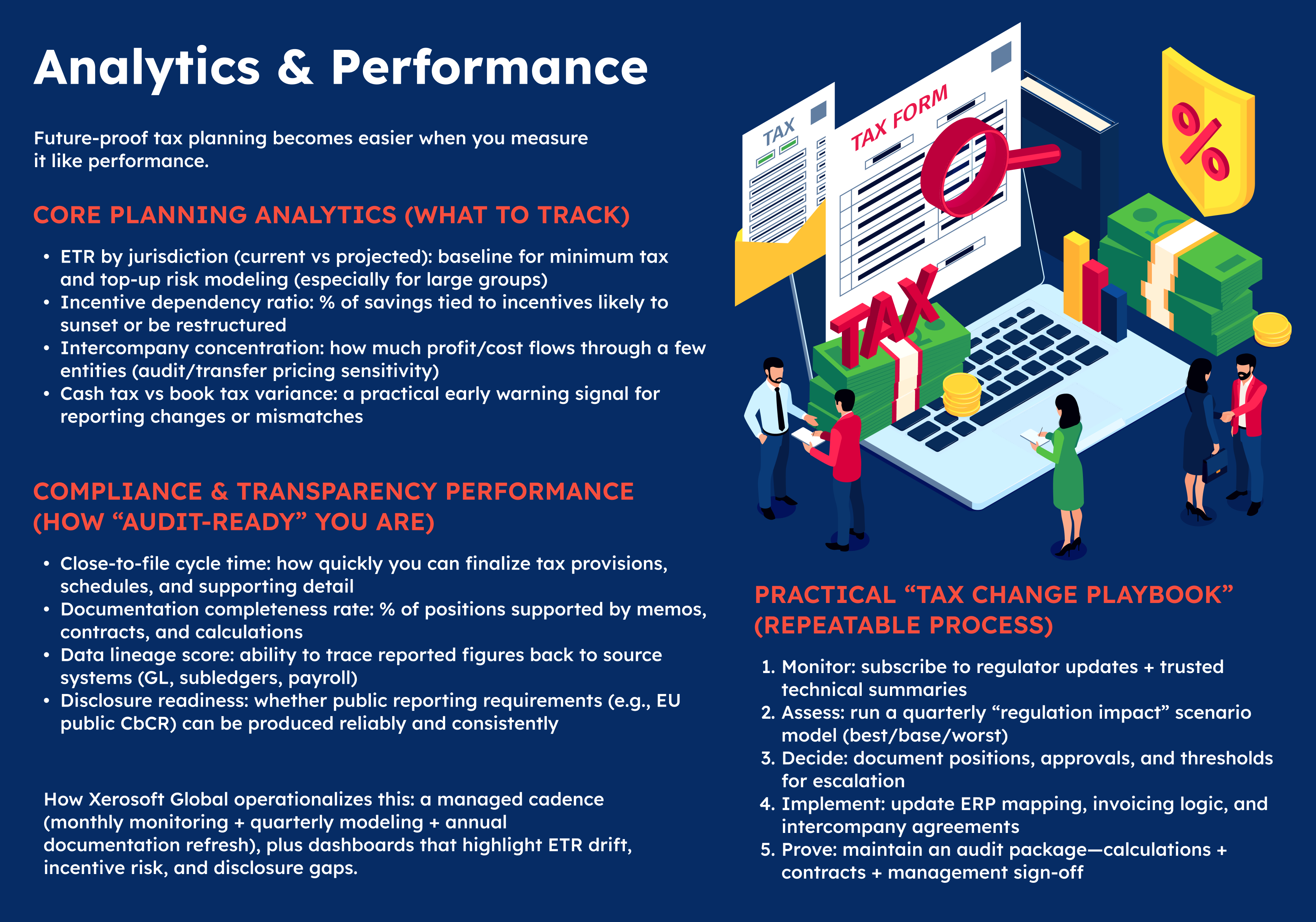

Reduced exposure to global minimum tax changes (Pillar Two)

Multinationals increasingly need to model effective tax rates by jurisdiction, evaluate top-up tax risk, and prepare for country-specific implementation. The EU has already required Member States to implement Pillar Two rules for fiscal years starting in 2024.

What this means for planning: entity structure, intercompany pricing, and incentive use must be stress-tested under minimum-tax mechanics—before expansion decisions lock in long-term consequences.

Better readiness for rising tax transparency requirements

Tax transparency is moving from “confidential filing” to “public scrutiny.” In the EU, public country-by-country reporting obligations require large in-scope groups to disclose tax and activity information publicly (with reporting requirements kicking in from 2026 on the EU’s own page).

Benefit: companies that standardize tax data early avoid rushed, inconsistent disclosures that create reputational and audit risk.

Faster adaptation when local rules diverge

Even when rules share a global theme (minimum tax, reporting, incentives), implementation varies country to country. Having a structured process—monitor, assess impact, update policies, and document decisions—prevents “fire drills” every time a jurisdiction updates guidance.

More confident expansion and investment decisions

Tax planning should support growth strategy: where to hire, where to sell, how to structure IP/licensing, and how to use incentives. In the Philippines, for example, corporate income tax rates differ depending on size thresholds, and minimum corporate income tax rules can apply—so planning needs to align with real operational profiles.

Where Xerosoft Global fits: Xerosoft Global can help build a tax planning operating model—entity mapping, policy design, documentation standards, and ongoing monitoring—so businesses don’t just “keep up,” they stay strategically prepared.

Conclusion

In 2026, corporate tax planning is less about one-time optimization and more about building a durable system that can withstand shifting rules: global minimum tax implementation, rising transparency demands, and jurisdiction-by-jurisdiction change. The companies that win treat tax as an operating discipline—powered by clean data, documented decisions, and measurable readiness. EU implementation timelines for minimum tax (Pillar Two) and expanding public disclosure expectations underscore why “future-proofing” can’t wait.

For businesses aiming to stay compliant, agile, and strategically positioned, Xerosoft Global can support the shift from reactive compliance to proactive tax governance—so regulation changes become manageable events, not disruptive surprises.

References

- European Commission — Minimum Corporate Taxation (Pillar Two implementation timeline)

- OECD — Central Record of Pillar Two Legislation (implementation tracking)

- European Commission — Public country-by-country reporting (overview and timing)

- Deloitte — EU Public CbCR applicability timing (member-state transposition + application window)

- PwC Tax Summaries — Philippines corporate income tax overview (rates and MCIT)