Payroll audits rarely start because a business is “big.” They start because something looks inconsistent: late tax deposits, misclassified workers, overtime errors, missing records, or mismatches between payroll reports and tax filings. The good news: most audit triggers are preventable with a disciplined checklist and tight controls.

Below is a practical payroll compliance checklist you can run every pay period, month, quarter, and year—built around the issues regulators most often scrutinize (late deposits, classification, recordkeeping, and reporting accuracy).

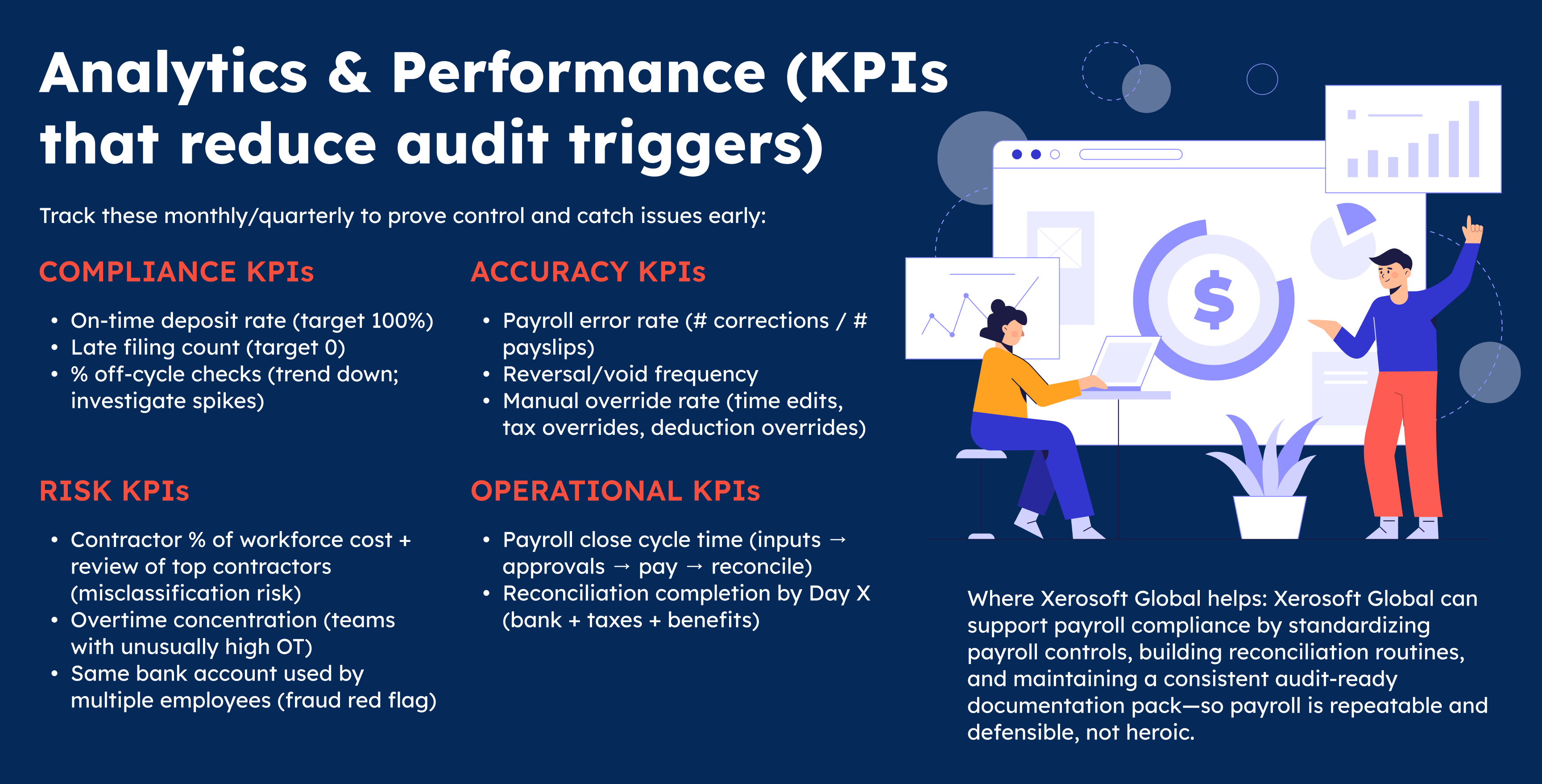

Key Benefits

Lower audit exposure and fewer penalty events

Late or incorrect payroll tax deposits are a classic trigger—and penalty rates escalate as delays grow.

Cleaner payroll data = faster, safer reporting

When payroll inputs (time, rates, deductions, employee status) are controlled, quarterly/annual reporting becomes reconciliation—rather than rework.

Better employee trust and fewer disputes

Accurate pay, correct overtime, and consistent deductions reduce complaints—another common “spark” that brings scrutiny to payroll processes.

Payroll Compliance Checklist (Anti–Audit Trigger Edition)

Foundational setup (Quarterly review or whenever you change process)

Worker classification + job setup

- ✅ Confirm employee vs independent contractor classification using your jurisdiction’s tests (misclassification is a major enforcement focus).

- ✅ Confirm exempt vs non-exempt (or equivalent) status and document the basis (job duties, salary thresholds, etc.). (US example: FLSA framework)

- ✅ Ensure job titles map correctly to pay rules: overtime eligibility, differentials, hazard pay, night shift rules, etc.

Payroll tax + statutory configuration

- ✅ Ensure withholding tables/rules are current and applied consistently (use official guidance where applicable). (US example: IRS Pub 15 outlines employer withholding/deposit/reporting responsibilities.)

- ✅ Confirm deposit frequencies and filing due dates are understood and calendared.

- ✅ Set up strong access controls: approvers, segregation of duties, audit logs, and change tracking.

Every pay run (Most common error zone)

Inputs and approvals

- ✅ Timekeeping approved (cutoff enforced; edits tracked with reason codes)

- ✅ Rate changes approved (promotions, step increases, COLA adjustments)

- ✅ New hires/terminations validated (start/end dates, final pay rules, benefits end dates)

Gross-to-net integrity checks

- ✅ Scan for anomalies:

- negative net pay

- duplicate employees / duplicate bank accounts

- unusual spikes in hours, bonuses, or deductions

- manual checks/off-cycle payments (high audit interest area)

- ✅ Overtime logic tested (especially blended rates, bonuses affecting OT base, and holiday rules). (Wage and hour compliance + recordkeeping are core FLSA obligations in the US.)

Documentation

- ✅ Maintain supporting documents for:

- pay changes

- allowances/benefits

- reimbursements

- deductions authorizations

- ✅ Ensure payroll registers are retained with the detail needed to support filings.

Monthly (or at minimum per filing cycle)

Deposit compliance (top trigger)

- ✅ Verify timely payroll tax deposits (late deposits can trigger penalties and scrutiny; penalty tiers can increase up to 15% depending on lateness and notices).

- ✅ Reconcile payroll tax liability accounts to filings and deposits.

Reconciliations that stop audits early

- ✅ Bank reconciliation: payroll clearing account ties to payroll register

- ✅ Tax payable reconciliations: withheld vs remitted

- ✅ Benefits reconciliation: employee deductions + employer contributions tie to invoices (and eligibility lists)

Quarterly (high-risk mismatch checks)

Filing accuracy + tie-outs

- ✅ Reconcile payroll totals to your quarterly employment tax returns (US example: Form 941 filing cadence + due dates).

- ✅ Check for consistency between:

- payroll registers

- quarterly returns

- year-to-date summaries

Classification and overtime recheck

- ✅ Review any role changes or manager reclassifications (exempt/non-exempt drift is common)

- ✅ Confirm contractor spend isn’t “employee-like” (schedule control, exclusivity, tools, supervision)

Year-end (where small mistakes become big problems)

Employee tax documents and annual summaries

- ✅ Ensure annual employee certificates/forms are complete and consistent with year totals.

- Philippines example: BIR Form 2316 is a key annual certificate; keep properly completed copies and align it to withholding reporting.

- ✅ Validate annual reconciliation across payroll system totals, statutory remittances, and filings.

Audit file package

Create a simple “payroll audit binder” (digital):

- payroll policies + approval matrix

- sample approvals (rate changes, bonuses)

- reconciliation reports (bank + tax payable)

- filings and remittance proofs

- exception logs and resolutions

Conclusion

Most payroll audits don’t uncover one giant fraud—they uncover repeatable process weaknesses: late deposits, classification errors, overtime/recordkeeping gaps, and filing mismatches. If you run the checklist above on a calendar rhythm (per pay run / monthly / quarterly / year-end), you reduce the most common triggers and make any review far easier to defend.