A clean corporate tax filing is rarely “won” in the final week. It’s won in the 90 days before the deadline—by locking down books, validating tax positions, and gathering documentation early enough to fix gaps without panic.

Below is a practical 30/60/90-day timeline that works across most jurisdictions (always confirm your entity type and local filing deadline).

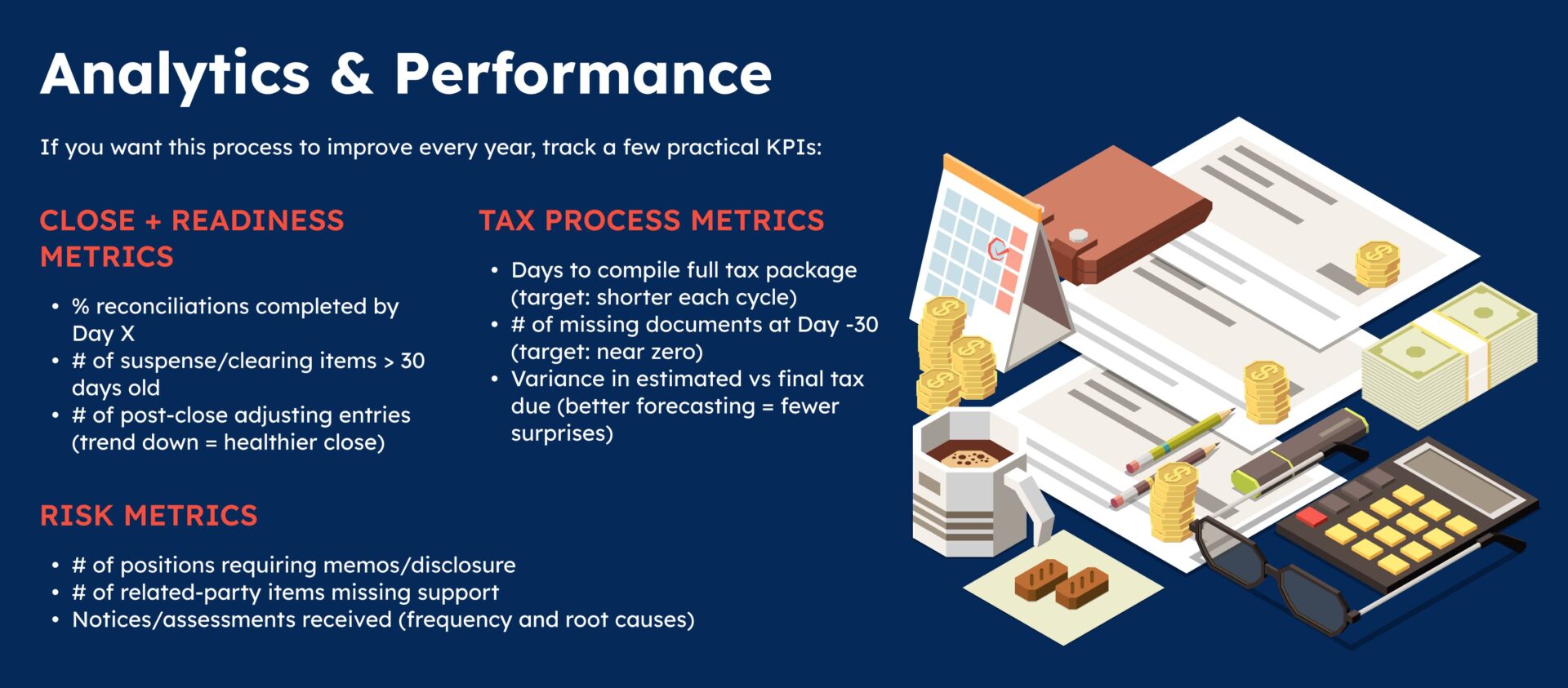

Key Benefits

Fewer surprises, fewer penalties

Preparing early reduces the two biggest causes of late/incorrect filings:

- Incomplete close (unreconciled accounts, missing accruals)

- Missing tax documentation (withholding certificates, intercompany support, fixed asset schedules)

Better tax outcomes (not just compliance)

Early prep gives you time to:

- Validate deductible expenses and substantiation

- Capture eligible credits/incentives

- Review timing strategies (income/expense recognition, provisioning)

Audit-ready support, even if you’re not audited

A strong filing package is basically an “audit file”:

- Clear support schedules

- Tie-outs from trial balance → tax return

- Documentation for significant estimates and judgments

90 Days Before Deadline

Lock your reporting scope

- Confirm legal entities included in the return (subsidiaries, branches, disregarded entities, partnerships where relevant)

- Confirm reporting currency and consolidation approach (if applicable)

- Identify any new registrations, closures, or restructuring events during the year

Stabilize your books (close quality first)

- Reconcile cash/bank, AR, AP, payroll, taxes payable

- Review suspense/clearing accounts (these often hide issues)

- Validate revenue recognition cutoffs (especially if you have long-term contracts or deferred revenue)

Create your “tax data room” checklist

- Prior-year tax return + assessments/notices

- General ledger / trial balance + financial statements

- Contracts that drive tax positions (leases, service agreements)

- Board resolutions, shareholder changes, dividend declarations (if any)

Flag high-risk areas early

- Related-party transactions and transfer pricing support (if applicable)

- Large unusual expenses (marketing spikes, consulting, repairs vs capex)

- FX gains/losses, impairment, provisions

- Any uncertain tax positions requiring disclosure or documentation

60 Days Before Deadline

Finalize core tax schedules (the “big rocks”)

- Fixed asset rollforward (additions/disposals, depreciation method/tax lives)

- Inventory reconciliation (if applicable)

- Accruals and prepaid schedules (timing differences)

- Loan schedules (interest, withholding, thin cap/interest limitation rules where applicable)

Validate deductibility + substantiation

- Ensure invoices/ORs/receipts are complete for material expenses

- Confirm proper classification (repairs vs capital improvements, employee benefits, representation/entertainment limits, etc.)

- Review intercompany charges: contracts + basis for allocation + proof of service

Run a pre-tax review (variance + reasonableness tests)

- Revenue and gross margin changes

- Major expense variances (by account)

- Effective tax rate movement (if you track it)

- Any “book-to-tax” reconciling items that look off

Decide early: file on time vs extension

If an extension is available in your jurisdiction, decide now (not at Day -3):

- What’s needed to file complete and accurate on time?

- If extending, what’s the estimated tax payment required to minimize interest/penalties?

30 Days Before Deadline

Tie-out and finalize the return package

- Tie trial balance totals to tax workpapers

- Confirm all adjustments have support (calcs, memos, source docs)

- Validate carryforwards (losses, credits) and limitations

- Confirm payments/withholding applied correctly

Finish compliance admin (the stuff that causes last-minute delays)

- Signatory authorization and e-sign setup

- Officer/director info, registered addresses, and IDs up to date

- Attachment requirements compiled (financial statements, schedules, disclosures)

Final review: accuracy + defensibility

- Review materiality thresholds and significant judgments

- Confirm consistency with statutory accounts (or document differences)

- Create an audit trail: “what changed vs last year and why”

Post-filing plan (don’t stop at submission)

- Save a complete filing archive (return + workpapers + supporting docs)

- Log learnings: top causes of adjustments + missing documentation

- Update next-year checklist so the next filing is smoother

Conclusion

The 30/60/90 approach works because it forces the right sequence:

- 90 days: stabilize books + identify risk

- 60 days: build schedules + validate substantiation

- 30 days: tie-out, review, sign, and file cleanly

Do this consistently and your corporate tax filing stops being a deadline crisis—and becomes a predictable, controlled finance process.