Corporate tax is no longer “just a finance topic.” In 2026, tax strategy, transparency, and controls increasingly sit inside the “G” in ESG—and stakeholders are connecting the dots between what companies say about sustainability and how they contribute through taxes, incentives, and governance. Regulations and standards are accelerating this convergence, especially in Europe (CSRD/ESRS) and through global tax initiatives like Pillar Two.

Key Benefits

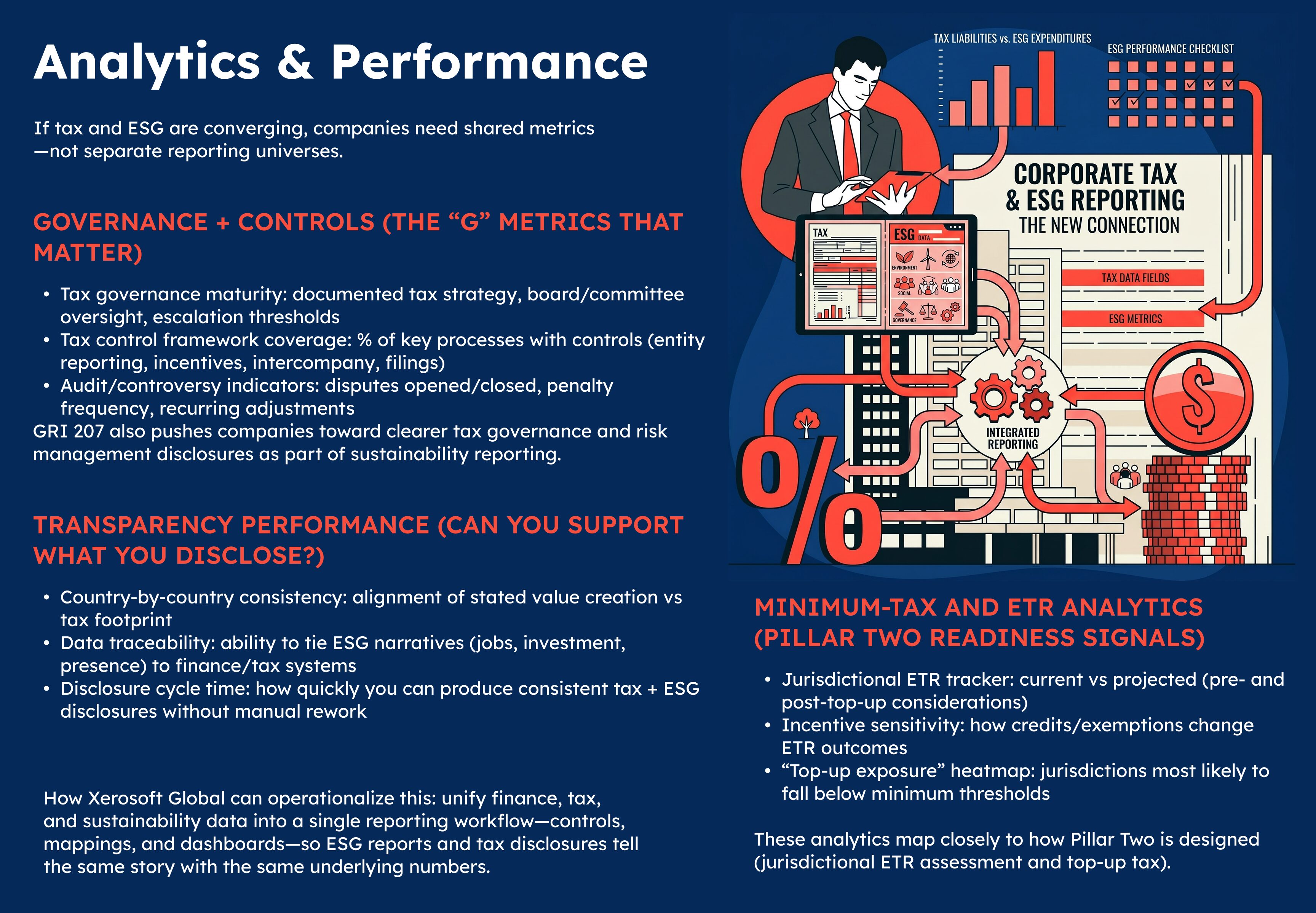

Stronger trust through tax transparency (the “G” gets real)

Tax behavior is becoming a reputational marker: boards, investors, and employees increasingly evaluate whether a company’s tax approach aligns with its public values. Frameworks like GRI 207 (Tax) explicitly support public disclosure of business activities and tax payments on a country-by-country basis.

Where Xerosoft Global fits: Xerosoft Global can help design a tax transparency narrative backed by data—so disclosures are consistent, defensible, and not “PR-forward but audit-weak.”

Better readiness for sustainability reporting requirements that touch tax

The EU’s CSRD requires in-scope companies to report using European Sustainability Reporting Standards (ESRS). While tax may not appear as a standalone line item everywhere, tax governance, business conduct, and value-chain impacts often pull tax-related data into scope through materiality and governance disclosures.

Fewer surprises as global minimum tax (Pillar Two) reshapes incentives and ETRs

The OECD’s Pillar Two (GloBE) framework introduces a jurisdictional effective tax rate test and a coordinated top-up tax mechanism toward a 15% minimum rate for in-scope multinational groups. This pushes companies to model ETR outcomes and document how incentives and structures affect tax results—information that stakeholders increasingly view through an ESG lens.

Cleaner assurance story across financial + sustainability reporting

Sustainability reporting is increasingly expected to be decision-useful and structured. The ISSB’s IFRS S1/S2 framework uses core pillars (governance, strategy, risk management, metrics & targets), which naturally intersects with tax risk management, controls, and disclosures when tax is financially material.

Conclusion

The connection between corporate tax and ESG reporting is now structural: tax transparency standards (GRI 207), sustainability reporting regimes (CSRD/ESRS), and global tax reforms (Pillar Two) are all pushing companies toward clearer governance, consistent disclosures, and defensible data.

Businesses that “future-proof” in 2026 treat tax as part of ESG governance—building strong controls, consistent metrics, and disclosure-ready data. Xerosoft Global can support that shift by helping organizations connect tax strategy, risk management, and ESG reporting into one coherent, auditable system.

References

- European Commission — Corporate sustainability reporting (CSRD/ESRS overview)

- GRI — Topic Standard for Tax (GRI 207)

- GRI — GRI 207: Tax 2019 (PDF)

- OECD — Global Anti-Base Erosion Model Rules (Pillar Two)

- OECD — Pillar Two GloBE Rules fact sheets (PDF)